[FORTUNE US=SHAWN TULLY]

The biggest fear by far haunting the worlds of business and investing is the I-word, short for the curse of looming inflation. Consumer and producer prices are waxing at their

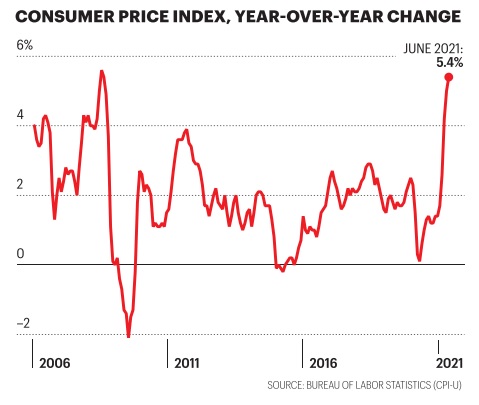

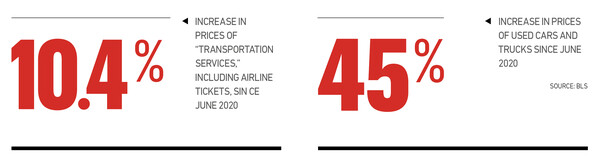

In June, the Bureau of Labor Statistics reported that consumer prices jumped by 0.9%, or 10.8% on an annual basis, and had risen 5.4% in the past 12 months, the highest reading since August 2008. Since June 2020, the cost of dining out has swelled by 4.2%, apparel by 4.9%, home energy by 6.3%, and “transportation services,” a category including airline tickets, by 10.4%. Used cars and trucks got a jaw-dropping 45% pricier, and at the gas station, you’re paying half again as much to fill your tank as a year ago.

Even Federal Reserve policymakers are predicting a swifter-than expected end to the run of ultralow interest rates that have fueled the boom: By mid-June the majority of top Fed officials believed that the Fed will raise rates twice by the end of 2023, a big reversal from the March outlook that called for increases in 2024 at the earliest.

Individuals and businesses don’t seem quite sure what to expect. A mid-June poll by Fortune and Momentive found that 87% of U.S. adults say they are concerned about inflation, up from 57% in our May poll.

However, the closely watched University of Michigan survey of consumers shows while inflation expectations for one year out are still high, they have begun to tail off for five-to-10 years out, perhaps adding credence to Fed Chairman Jerome Powell’s stated view that the inflation we’re seeing is “transitory.” Amid the baffling array of numbers and possible scenarios, there are three important things to understand about how inflation is playing out in the economy.

MYTH NO. 1

Inflation is universally bad

Inflation is like drinking—it’s fine in moderation, but disastrous when extreme.

Almost all economic expansions are accompanied by rising prices. But production shortages (in this case caused by COVID-19) and the Fed’s easy money policies suddenly mean more dollars chasing fewer goods, which is what leads to inflationary pressure. Inflation between 1% and 3% is considered fine. But when prices start spiking 4% or 6% or more, it can be dangerous. First, companies may be locked into contracts that require them to deliver goods at fixed prices, whereas their suppliers are free to charge more for components immediately. That scenario could squeeze profit margins.

Second, high inflation makes shareholders wary of government policies and what the future holds. They’ll demand higher returns for stocks versus safe bonds than in most periods, so they are less willing to buy stocks at the sky-high price/earnings ratios that have characterized the market recently. Runaway goods prices would sharply reduce what investors are willing to pay for each dollar of earnings, driving the indexes down steeply.

For bonds, inflation is mostly bad, unless you’re in TIPS (Treasury Inflation-Protected Securities), whose value rises with overall prices, keeping investors whole.

For homeowners, more inflation would most likely be a boon. The rate on the classic 30-year mortgage stands near multi-decade lows at 2.74%. That’s only slightly above the projected rate of inflation of around 2.3% for the next decade. If the consumer price index

(CPI) were to rise to 3% or 4%, homeowners would probably get raises in line with the rising cost of living. They would have more dollars to make a monthly interest nut that’s fixed.

But the player that will fare worst in a high inflationary environment? Uncle Sam. “The Treasury is borrowing to finance the deficits at what amounts to the kind of short-term teaser rates that folks who bought houses in 2006 took out, thinking their homes’ values could only increase,” says John Cochrane, an economist at the Hoover Institution. He fears that a jump in rates on the huge amounts of debt the Treasury is forced to roll over each year could push interest expense to unsustainable heights, unleashing a crisis. “You will see

intense pressure to keep rates low,” he says. “If they go up too much, you’ll have too-big-to-fail banks, a budget meltdown, and a lot of equity investors who will lose a lot of money.”

MYTH NO. 2

Prices are the best inflation gauge we have

There’s a road map to where rates are headed—but you have to know where to look. Since bonds are so exquisitely sensitive to the threat of inflation, the yield curve represents “the summary of the market’s best estimates,” says Bruce Sherrick, an agricultural economist at the University of Illinois.

The yield curve is simply the line linking the dots that mark the current yields on Treasuries

of all maturities. On a recent day, the slope starts low and superflat at the one-month bill, paying a minuscule 0.04%, rising to the one-year at 0.08%, then to the two-year (0.24%), three-year (0.44%), five year(0.81%), on to the benchmark 10-year at 1.27%, and finishing at the 30-year (1.90%).

What’s mostly ignored is the forecast embedded in the curve. Both one year and five-year rates are historically low right now. But when the five year yield is many, many multiples of the one-year yield, as it is now, that’s often a predictor of inflation and fast-rising short-term rates ahead. “The yield curve shift is signaling something that is really important,” says Cochrane. Adds Sherrick, “We’re seeing higher expectations for inflation than a few weeks ago.”

MYTH NO. 3

The Fed is totally in control

Yes, the Fed has many levers at its disposal. But there are limits to how much it can control.

Let’s back up. Behind the scenes, the Fed has been playing a neat trick with the economy. It’s been described as “stepping on the gas when the car’s in neutral.” Prior to the Great Financial Crisis, the Fed didn’t pay interest on the “reserves” or deposits it holds for banks. But since late 2008, it’s been offering rates that, though seemingly low, are so attractive that banks have been leaving the lion’s share of the freshly issued money as reserves. Since

2008, bank reserves at the Fed have exploded from $900 billion to $8.2 trillion, with over half the increase coming since the onset of COVID-19.

“The strategy is to pay premium rates to sequester that extra money at the Fed and prevent it from leaking out into new lending,” says William Luther, an economist at Florida Atlantic University. If the Fed had allowed those trillions to fund new loans, inflation would have rampaged. Instead, the new money went to two causes: first, supporting big deficits and the COVID stimulus; and second, raising the capital cushions that have made commercial banks extra safe.

The Fed clearly doesn’t want to see 3% or 4% inflation. Still, a measure called the 10-year breakeven inflation rate, based on the yield for inflation protected bonds, forecasts 2.3% price increases in the decade ahead, already above the Fed’s target. “We get price information with a lag,” says Luther. “If we see more big inflation numbers, companies will start charging higher prices in long-term contracts, and workers will demand bigger raises in their agreements. When inflation gets out of hand, it happens fast. It would take strong political will to wrestle it down.” As economist Larry Summers warned recently, “The Fed has had almost no success in bringing down prices once the economy has overheated.”

The most likely scenario is that the Fed keeps paying interest on deposits, and that the policy of blocking the gigantic increases in the money supply from flowing to easy credit succeeds. But it’s not the only scenario. As Summers reminds us, the only real cure for runaway inflation is a painful one: reining in credit and causing a recession. That’s the big threat to America’s powerful reopening comeback—and one the Fed will have to navigate carefully.

[FORTUNE US=SHAWN TULLY]